When it comes to retirement savings, understanding the nuances of spousal Roth IRA contributions can significantly enhance your financial future. Many couples are unaware of the benefits and strategies associated with spousal contributions, which can optimize their retirement savings and tax advantages. This article will guide you through everything you need to know about spousal Roth IRA contributions, providing expert insights and practical tips.

In today's financial landscape, making informed decisions regarding retirement accounts is crucial for ensuring long-term financial stability. A spousal Roth IRA allows a non-working spouse to contribute to a retirement account, which can lead to substantial growth over time. This guide aims to demystify the rules, benefits, and strategies associated with spousal Roth IRA contributions.

Whether you're just starting your retirement planning journey or looking to maximize your existing accounts, understanding how to effectively utilize spousal Roth IRAs can make a significant difference. Read on to discover how you can leverage this financial tool for a secure retirement.

Table of Contents

- What is a Spousal Roth IRA?

- Eligibility Requirements for Spousal Roth IRA Contributions

- Benefits of Spousal Roth IRA Contributions

- Contribution Limits for Spousal Roth IRA

- How to Contribute to a Spousal Roth IRA

- Tax Implications of Spousal Roth IRA

- Strategies for Maximizing Spousal Roth IRA Contributions

- Conclusion

What is a Spousal Roth IRA?

A spousal Roth IRA is a type of retirement account that allows a working spouse to contribute to a Roth IRA on behalf of a non-working spouse. This account is especially beneficial for couples where one partner earns an income while the other does not. By contributing to a spousal Roth IRA, the couple can effectively increase their retirement savings and take advantage of the tax-free growth offered by Roth IRAs.

Key Features of Spousal Roth IRA

- Tax-free withdrawals in retirement

- No required minimum distributions (RMDs) during the account owner's lifetime

- Contribution flexibility for couples

Eligibility Requirements for Spousal Roth IRA Contributions

To contribute to a spousal Roth IRA, certain eligibility criteria must be met. These include:

- The couple must file a joint tax return.

- The working spouse must have enough earned income to cover the contribution for both spouses.

- The non-working spouse must be below the age limit for Roth IRA contributions.

Benefits of Spousal Roth IRA Contributions

There are several advantages to contributing to a spousal Roth IRA:

- Enhanced Retirement Savings: Allows for additional contributions, increasing overall retirement savings.

- Tax Advantages: Contributions grow tax-free, and qualified withdrawals are also tax-free.

- Financial Independence: Provides a safety net for the non-working spouse, contributing to their financial security.

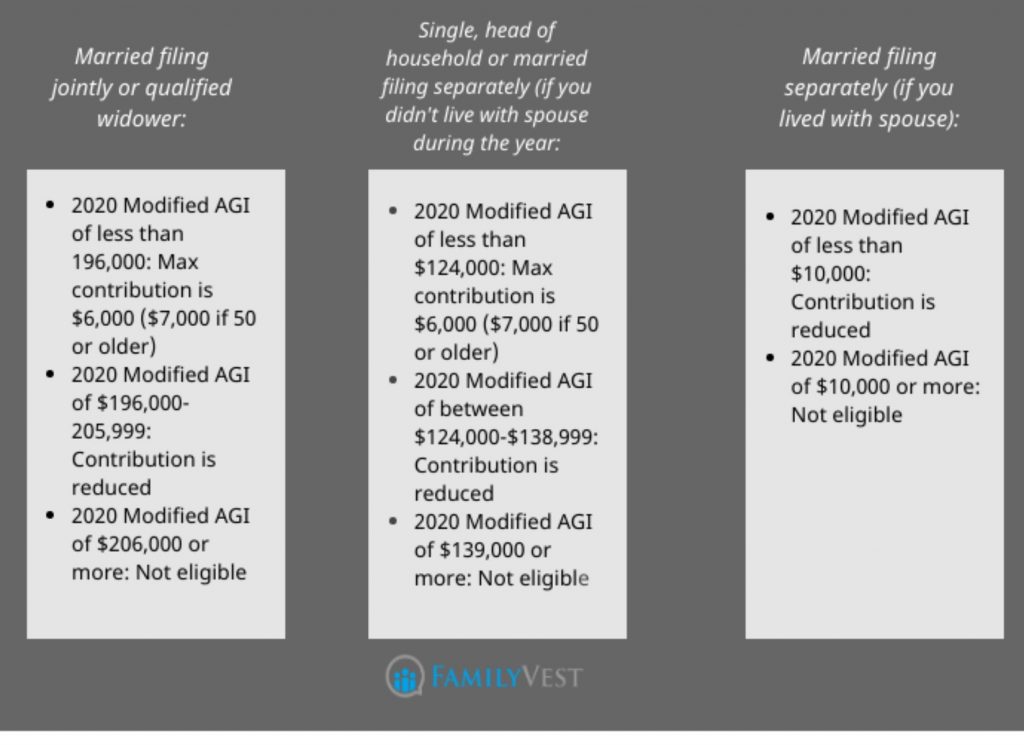

Contribution Limits for Spousal Roth IRA

For 2023, the contribution limit for Roth IRAs, including spousal contributions, is $6,500 per person, or $7,500 for those aged 50 and above. However, the ability to contribute phases out at higher income levels. The following outlines the income limits:

Income Phase-Out Ranges

- Married filing jointly: $218,000 to $228,000

- Married filing separately: $0 to $10,000

How to Contribute to a Spousal Roth IRA

Contributing to a spousal Roth IRA involves a few straightforward steps:

- Open a Roth IRA account for the non-working spouse.

- Ensure that the working spouse’s income is sufficient to cover the contribution.

- Make contributions directly to the non-working spouse’s Roth IRA account.

Tax Implications of Spousal Roth IRA

Understanding the tax implications of spousal Roth IRA contributions is vital for effective financial planning:

- Contributions are made with after-tax dollars: This means that the contributions do not reduce your taxable income.

- Qualified withdrawals are tax-free: This applies to both contributions and earnings if taken after age 59½ and the account has been open for at least five years.

Strategies for Maximizing Spousal Roth IRA Contributions

Here are some strategies to consider when aiming to maximize contributions to a spousal Roth IRA:

- Maximize contributions early in the year to take advantage of compounding interest.

- Consider using existing savings to fund contributions if cash flow is tight.

- Review contribution limits annually to ensure compliance and maximize potential savings.

Conclusion

Spousal Roth IRA contributions present a valuable opportunity for couples to enhance their retirement savings strategy. By understanding eligibility requirements, contribution limits, and tax implications, couples can leverage this financial tool effectively. If you haven’t already, consider consulting a financial advisor to explore how a spousal Roth IRA can fit into your retirement planning.

If you found this article helpful, please leave a comment below or share it with others who may benefit from understanding spousal Roth IRA contributions. Don’t forget to check out our other articles for more insights on retirement planning and financial strategies.

Thank you for reading! We hope to see you back here soon for more valuable financial advice and tips.

You Might Also Like

Doug Bailey: The Man Behind The Visionary IdeasHeart Of The Elements Calamity: A Deep Dive Into The Mystical Realm

U-Haul Storage In Rogers, AR: A Comprehensive Guide

DMV Rahway NJ: Your Comprehensive Guide To Services And Processes

Understanding Planet Fitness Annual Fee: What You Need To Know

Article Recommendations